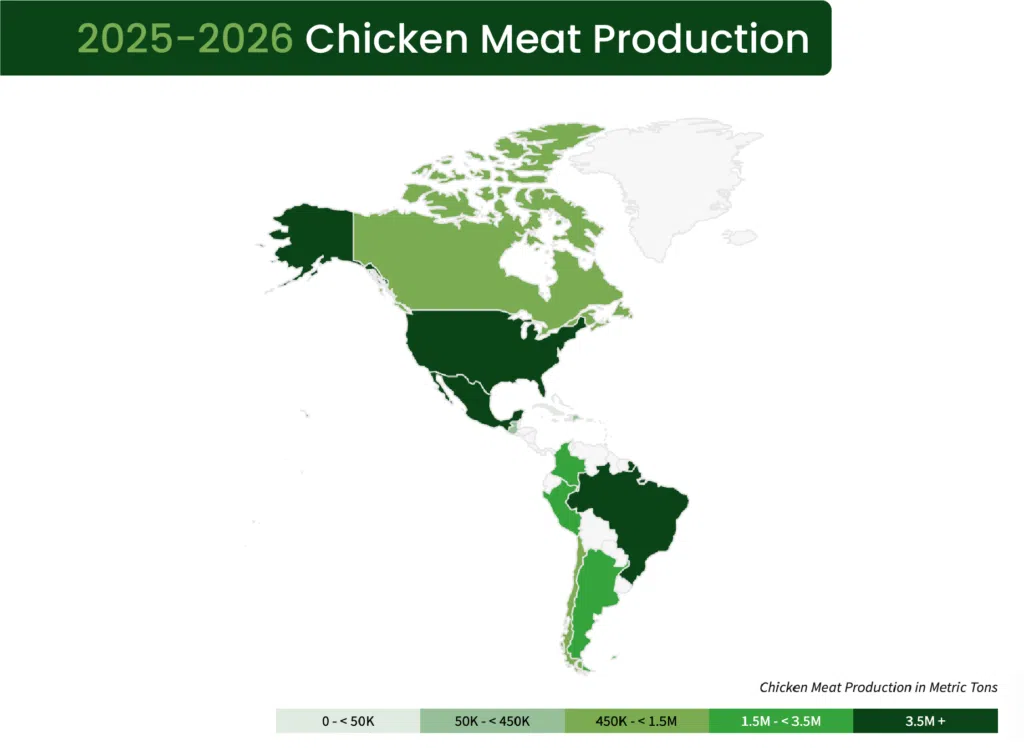

The Americas produced more poultry in 2025 than at any point in history. Broiler output in the United States topped 48 billion pounds while Brazil shipped record volumes to markets across five continents. Mexico’s feed industry hit a new high. Across the continent, from Colombia and Peru to Argentina and Chile, the sector kept expanding. But the numbers only tell part of the story. Behind this growth, producers are facing growing pressure from multiple fronts: disease outbreaks, geopolitical instability, trade volatility, evolving regulations, and shifting consumer demands. What makes this region compelling right now is not just the scale of production. It is how fast the landscape around it is changing.

Credits: USDA Foreign Agricultural Service (U.S Department of Agriculture)

More Birds, More Eggs, and a Changing Landscape

U.S. broiler production grew 2% in 2025, with the USDA projecting another 1% for 2026 on lower feed costs and resilient demand. The market was valued at approximately USD 41 billion, with chicken accounting for 88% of all poultry volume consumed. In Brazil, close to 5.5 billion broilers were produced in 2024, and the USDA forecasts record levels for 2026 as input costs fall and the country recovers access to key export markets. Mexico is approaching the 2 billion broiler mark, supported by a feed sector that produced 41 million metric tons in 2024, nearly half of it directed to poultry.

The egg sector tells an equally compelling story. In 2024, Latin America’s per capita egg consumption surpassed the global average for the first time, reaching 292 eggs per person versus 271 worldwide, according to the Latin American Egg Institute (ILH) and the Latin American Poultry Association (ALA). Some highlights across the region:

- Mexico leads globally at 394 eggs per capita, home to six of the ten largest egg companies in the region, including Proan (41 million layers, second largest in the world) and Bachoco.

- Brazil’s layer sector exceeded 57 billion units in 2024, with companies like Global Eggs and Granja Mantiqueira consolidating through major acquisitions domestically and internationally.

- Colombia (343 eggs per capita), Argentina, Peru, the Dominican Republic, and other markets across the region are all posting steady growth.

Taken together, the region now accounts for more than 12% of the world’s total egg output, a figure that continues to climb year over year.

The Risks That Travel With Growth

This expansion is not happening without friction. Several pressures are converging, and understanding them is essential for anyone making production or nutrition decisions in the region today.

Disease as a structural risk. HPAI has gone from a periodic disruption to a recurring pattern across the hemisphere. In the U.S., outbreaks in late 2024 and early 2025 affected over 60 million layers, driving wholesale egg prices to USD 8.53 per dozen before they collapsed to around USD 1.12 by year-end. In Brazil, HPAI detections in mid-2025 temporarily restricted commercial export access. Each cycle carries a cost in lost capacity, market instability, and the resources required to rebuild.

Geopolitics, conflict, and supply chain fragility. Ongoing global conflicts and trade tensions are adding pressure to input costs and logistics across the Americas. Grain and energy markets remain sensitive to geopolitical disruptions, and freight costs have been volatile as shipping routes face recurring instability. Closer to home, Mexico depends on U.S. suppliers for over 95% of its imported yellow corn, a concentration that any tariff shift or trade policy change could expose. Brazil’s export strength is real, with 3.2 million metric tons of chicken shipped in the first eight months of 2025, but maintaining access to over a hundred markets requires constant alignment with shifting sanitary and trade frameworks.

The antibiotic equation. In the U.S., medically important antibiotics for growth promotion have been banned since 2017, and since June 2023 all purchases require a veterinary prescription. The FDA reports a 36% drop in antimicrobial sales for livestock since 2015. USPOULTRY data shows hatchery antibiotic use in broilers fell from 90% in 2013 to less than 1% by 2023. In Latin America, Argentina, Colombia, and Chile have restricted growth promoters classified as critically important by the WHO, and Brazil is progressively tightening its framework. The direction is the same everywhere: fewer chemical tools, higher production targets, and consumers who are paying attention.

Where Natural Ingredients Enter the Picture

This convergence of pressures is reshaping how producers and nutritionists approach feed programs. The global phytogenic feed additives market, valued at approximately USD 1.1 billion in 2025, is projected to approach USD 1.8 billion by 2032, with North America growing at a CAGR of 9%. Plant-derived ingredients are no longer a niche. They are becoming a structural part of production strategies across the Americas.

Among these, Quillaja saponaria extract is one of the most extensively studied bioactive ingredients available to the poultry industry. Its triterpenoid saponins work through well-documented and interconnected biological pathways:

- They bind cholesterol in pathogen membranes, directly disrupting the integrity of key enteric organisms.

- They activate innate immune responses, including macrophage function, cytokine production, and both cellular and humoral immunity.

- At the gut level, they strengthen villus structure, tight junction integrity, and nutrient absorption.

These mechanisms do not act in isolation. They reinforce each other, which is why the ingredient performs consistently under real production conditions where birds face simultaneous challenges from disease pressure, dysbiosis, stress, and environmental variability. Research has documented these effects across broilers, pullets, layers, and breeders, with measurable outcomes in growth, feed conversion, mortality, egg production, and eggshell quality. Available as an ingredient across all American markets, Quillaja saponaria extract offers formulators and integrators a proven, multi-functional option for programs that need to deliver performance while adapting to a rapidly changing landscape.

Looking Ahead

The poultry industry across the Americas is entering a phase where growth alone is not the measure of success. The producers and companies that will lead the next chapter are the ones building resilience into their operations today: through smarter nutrition, better risk management, and ingredients that deliver across multiple fronts. The challenges are real, but the region has the scale, the talent, and the tools to meet them.

References

1. USDA Foreign Agricultural Service. Livestock and Poultry: World Markets and Trade. December 2025.

2. USDA Economic Research Service. Livestock, Dairy, and Poultry Outlook: January 2026 (LDP-M-379).

3. Mordor Intelligence. United States Poultry Meat Market Size & Growth to 2031. January 2026.

4. WATTPoultry / B. Ruiz. Latin America’s Top Broiler & Layer Producers 2024. May 2025.

5. Latin American Egg Institute (ILH) / Latin American Poultry Association (ALA). 2024 LATAM Productive Data Report.

6. Feedstuffs / USPOULTRY. Antibiotic stewardship in U.S. poultry production progresses. December 2024.

7. Cardoso-Ugarte GA, et al. Regulations on the Use of Antibiotics in Livestock Production in South America. Antibiotics. 2023;12(8):1303.

8. Grand View Research. Phytogenic Feed Additives Market Size | Industry Report 2030.

9. Blue CEC, et al. Inclusion of Quillaja Saponin Clarity Q Manages Growth Performance, Immune Response, and Nutrient Transport of Broilers during Subclinical Necrotic Enteritis. Microorganisms. 2023;11(8):1894.

10. Fleck JD, et al. Saponins from Quillaja saponaria and Quillaja brasiliensis: particular chemical characteristics and biological activities. Molecules. 2019;24(1):171.